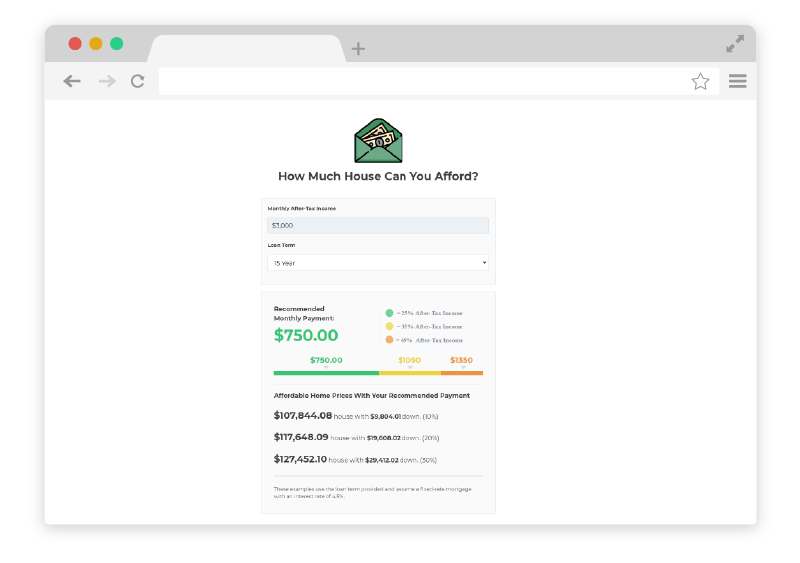

Use this calculator to estimate an affordable monthly payment based on your monthly after-tax income.

Go to Affordability Calculator

Whether you’re a first-time home buyer or a seasoned homeowner, this step-by-step guide contains everything you need to get a loan you love and a home that fits your budget.

Get Your Free Guide